Global Market Review

Share this article

Global automotive market report - Q1 2019

The global vehicle market was virtually flat in 2018 at around 94m vehicles sold, but the fourth quarter showed a near 5% year-on-year drop on the back of a similarly sized decline in Q3. The global light vehicle market continues to face challenges in 2019 after that pronounced weakening in the second half of 2019.

Overall

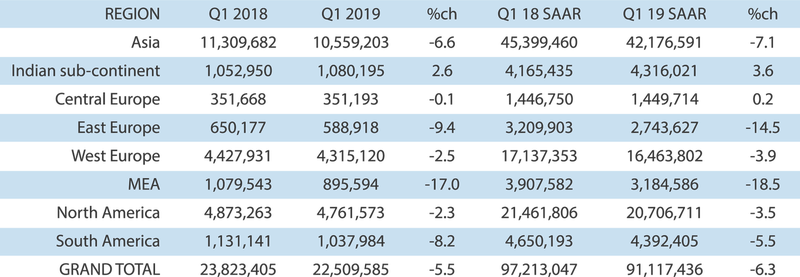

Our analysis shows that the first quarter showed declines to vehicle demand in most regions of the world as economies slowed and business and consumer confidence stalled. Overall Q1 vehicle sales were down 5.5% at 23.8m units. The Q1 seasonally adjusted annualised running rate (SAAR) was down 6.3% at 91.1m units. It was a story of decline across most of the world's regions.

China's car market declined following a combination of regulatory tightening to rein in shadow banking and an increase in trade tensions with the US which sapped confidence.

The euro area economy lost more momentum than was expected with some hangover from the disruption to car production in Germany caused by the introduction of new WLTP emission standards. Investment dropped in Italy with recession threatened.

Although there have been hopeful signs of conditions easing in 2019, with interest rates staying low in the US and more optimism over the prospects of a US-China trade deal, some of that optimism has waned as it has become clearer that US-China trade negotiations have hit obstacles (and tensions have been ramped up with recent tariff increases).

The IMF, in its latest economic projections, notes that the global economic growth peaked at close to 4% in 2017, before weakening to 3.6% in 2018. It is projected to decline further to 3.3% in 2019 and it says that the outlook for many countries is very challenging, with considerable uncertainty in the short-term.

After declining in 2018, the outlook for the global light vehicle market in 2019 is for a further decline. A deterioration to the demand trend in the second half of 2018 continued into the first quarter and it looks likely that the global market this year will be weighed down by lower sales in major automotive markets − especially the US, China and Europe.

US market shows volatility

The US vehicle market this year has seen considerable volatility. The early part of the year was depressed by severe winter weather, lower tax refunds and the effects of the US federal government shutdown. Thereafter, there was something of a recovery with overall market results surprising on the upside in February and March. Nevertheless, US deliveries of light vehicles were down 3.3% in the first quarter of 2019 as March volume fell 3.2%. Some impetus to the market could come from new product actions later this year and most analysts note that the US economy's fundamentals − low interest rates, low unemployment, low inflation − should continue to support a relatively high, by historical standards, market of 16.6-16.8m units (compares with 17.3m units in 2018). However, confidence could take a hit if the trade war with China flows into higher prices for consumer goods.

China concerns brewing

The path of China's economy and the trade spat with the US continues to cause concern in the automotive sector.

The path of China's economy and the trade spat with the US continues to cause concern in the automotive sector. Besides sourcing and supply-chain headaches caused by the threat of new tariffs, car demand is looking weak and also vulnerable to bad economic news.

First quarter total vehicle sales fell by 12.6% to 5.76m units from 6.59m units in the same period of last year. However, the rate of decline slowed in March. New vehicle sales in China fell by 5.2% to 2.52m units in March from 2.66m units a year earlier. It was though, the ninth month in succession that China's vehicle market has been in negative territory. An overhang of built up stock is partly responsible for slow wholesale deliveries in the early part of 2019.

The Chinese auto industry trade association, CAAM, hopes to see a turnaround in the second half of the year. Discounting activity could help shift high stocks and boost retail volumes, analysts say. The Chinese government has also introduced stimulus measures to help lift domestic consumption, including a cut in the manufacturing VAT rate from 16% to 13% at the beginning of April. It has also loosened monetary policy this year, including measures to encourage bank lending.

One positive development is buoyant sales of new energy vehicles (NEVs) − which rose by 85% to 126,000 units in March, driven by the introduction of minimum sales quotas at the beginning of the year.

The outlook for the rest of the year is far from bullish and somewhat jittery though. Beijing is wary of major economic stimulus measures as it works to reduce worryingly high debt levels in the Chinese economy. And the trade tensions with the US, which had seemed to be easing, could be ratcheted up again. In the mix though, Beijing is also very sensitive to the dangers of too sharp an economic slowdown. If the economy looks to be slowing more rapidly than the government plans, a public sector led stimulus would be very tempting to policymakers − even given the risks of a financial instability due to even higher debt levels.

Europe tracks down

In Europe, the first quarter's car market was a sluggish one. Vehicle sales in Western Europe were down by 2.5%. The car market alone in Western Europe was off by around 3.5% on last year's pace. Economic data continues to disappoint. Germany's economy has seen economic output stagnate and lose momentum following disruption to vehicle manufacturing in the second half of 2018. Italy has been close to recession. Other countries are also depressed, businesses and consumers sapped of confidence in conditions of some uncertainty. Brexit − and its associated uncertain path and macro effects − has also been a factor in reinforcing negative sentiment.

Most of the region's markets showed negative sales trends in the first quarter and − given that the market is running at a historically high level (Western Europe's car market could still be close to 14m units in 2019) − it's hard to see the rest of the year making up for a sluggish first half. A bounce-back in Germany − its economy and car market − would be a big help.

Another ongoing − and market depressing feature − is diesel share decline and uncertainty over policy directions. Diesel car sales are on the wane in Europe and that also translates into a softer market because many diesel car owners are putting off replacement purchases in the absence of clear signals from policy makers on how diesel cars will be treated in regulatory and tax terms. Nowhere is the rapid decline of the diesel passenger car more evident than the UK, where the diesel share of the car market fell to just 32% in 2018, compared with 42% in 2017. It is showing signs of stabilisation now, but diesel car owners holding off from replacement is an ongoing negative − especially with electrified low-CO2 (and low fuel consumption) alternatives still at a relatively early stage of market introduction.

India provides some Q1 cheer

India's economy is performing relatively strongly in 2019 and that's creating the right conditions for some market growth (India is the main market providing the positive figure for the Indian sub-continent in our table below). According to the IMF's latest projections, economic growth is projected to pick up to 7.3% in 2019 and 7.5% in 2020, supported by the continued recovery of investment and buoyant consumption amid a more expansionary stance of monetary policy and some expected impetus from fiscal policy − general election results notwithstanding.

According to the trade body Society of Indian Automobile Manufacturers (SIAM), total passenger vehicle (cars and SUVs) rose 2.7% to 3,377,436 units in the fiscal year ended March 2019. However, there was some slowdown in the second half. This year, the second quarter is likely to be off to a hesitant start with the Indian vehicle market adversely impacted by a combination of political uncertainty, higher insurance premiums, raised fuel prices, tight credit conditions and general upward pressure on vehicle prices. Much depends on the short-term economic path that emerges after the general election, but the latter part of 2019 could see confidence return and a bounce-back to economic growth that would support India's car market. The latter part of the year also sees the festive season. In addition, a tightening of emissions standards could create some pull forward of car demand supported by manufacturer promotions.

Elsewhere around the world the world the picture is rather downbeat in the early part of 2019. New vehicle sales in southeast Asia's six largest markets combined increased by 1.9% to 853,383 units in the first quarter of 2019 from 837,481 units in the same period of last year. This represents a marked slowdown from the 6.0% growth seen in the whole of last year and reflects a sharp decline in one of the region's largest markets. Sales in Indonesia fell by 13% to 253,863 units in the first three months of the year, reflecting sluggish economic growth and a degree of uncertainty ahead of the presidential and parliamentary elections held in April.

The Japanese light vehicle market decelerated sharply for the third consecutive month in March. The March market was down 3.6% on last year and analysts note that the positive impact of the number of major new model launches over the past year has diminished.

In South America, first quarter 2019 vehicle sales in Brazil improved 11.4% compared to the same period last year, reaching 607,600 registered units versus 545,500 in 2018. The economic picture is relatively positive in Brazil, with hopes high for a moderate recovery continuing despite some ongoing political instability. The IMF projects that brazil's rate of economic growth will strengthen from 1.1% in 2018 to 2.1% percent in 2019. It's a significantly less positive situation in neighbouring Argentina where the economy remains gripped by crisis. Argentina's economy is projected to contract in the first half of 2019 as domestic demand slows with tighter policies to reduce imbalances, returning to growth in the second half of the year as real disposable income recovers. In the first quarter, Argentina's light vehicle market plummeted by almost 50% to around 133,000 units.

In the other big BRIC market, Russia, sales so far this year suggest continuing market stagnation amid sluggish economic growth. The IMF projects economic growth for Russia of about 1.5% per annum over the medium term, weighed down by the modest outlook for oil prices and structural headwinds for the Russian economy. Russia's light vehicle market was virtually flat on last year during the first quarter as Russia's economy continues to experience slow growth. AEB figures suggest a 21% market share in Q1 for Lada, sales up 4% on last year. Russia's indigenous carmaker is nothing if not resilient in the face of tough market

Conditions.

First quarter light vehicle sales and SAARs by region